As part of our ‘Researching Africa in the 21st Century’ course, we – master’s students ‘African Studies’ at Leiden University – were all asked to work on a collaborative project that would incorporate multimodal and mixed-method field research about African societies in The Netherlands – The Hague in particular.

Sandra Bleeker, Mira Demirdirek and I decided to work together on a research project on the social significance of remittances being received from and sent to the African diaspora in The Netherlands.

In recent years, there has been a growing interest in the developmental potential of (international) money transfers by policy makers as well as academics. However, the phenomenon of remittances is usually being researched from an economic or political standpoint. We decided to approach it from a slightly different angle and look into the social aspect of remittances instead, by organising several interviews, conducting a questionnaire and creating an interactive map to give people an insight into where all the different money agents in The Hague are located.

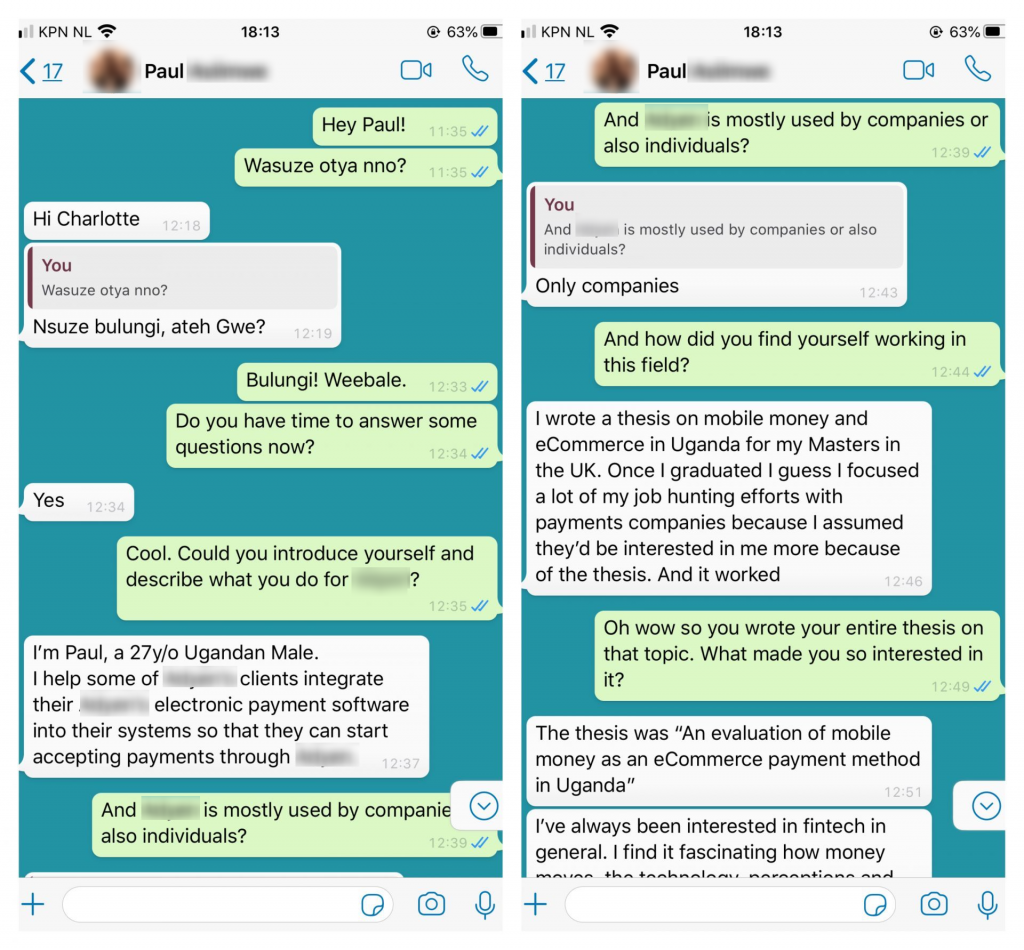

After having interviewed Abiola together with Mira (click through to view that particular blog post), I was trying to find someone who was knowledgeable on the more technical sides of remittances and the social impact that the technology behind it has had. That’s how I eventually got in touch with Paul (who would prefer to further remain anonymous), a Ugandan national who mostly resides in Amsterdam (although he still spends a lot of time in Uganda) and works for a Dutch global payment company that allows businesses “to integrate electronic payment software into their systems”, in Paul’s own words. Through Facebook Messenger, he called himself “a payments nerd”, so I knew I had stumbled upon the right person.

I had initially planned on visiting Paul in Amsterdam and interviewing him using a video recorder, but circumstances made that impossible and we instead decided to conduct the interview through WhatsApp, which worked well.

The interview can be read below.

For privacy reasons, I have removed Paul’s surname and employer from the conversation.

Paul made some very interesting points, which I have summarised below.

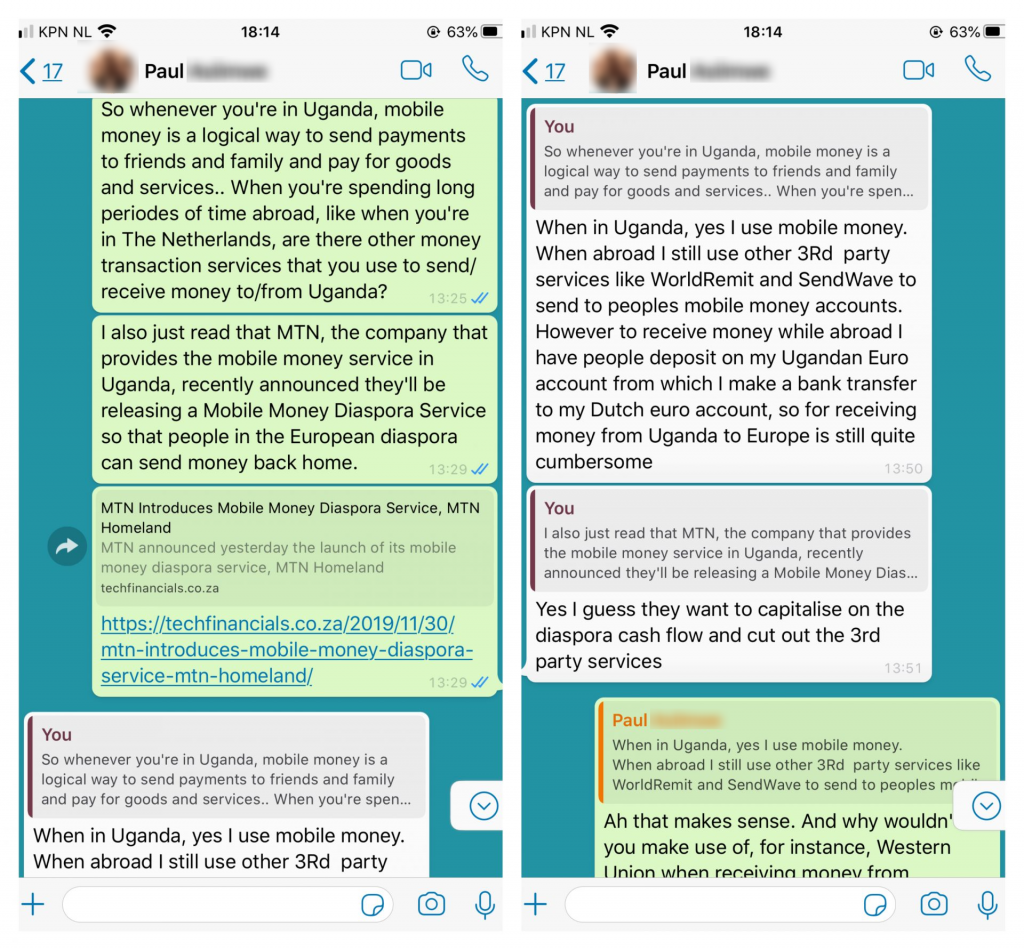

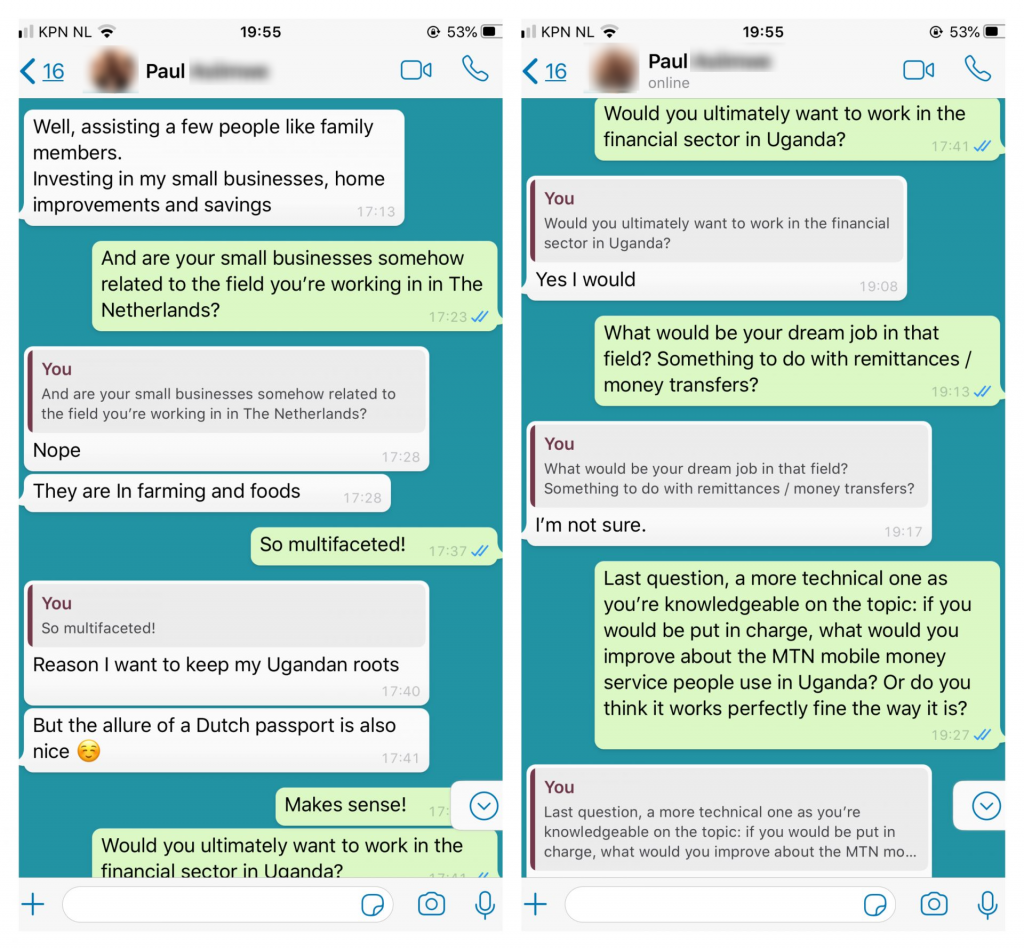

- While Abiola still receives most of her payments through Western Union by visiting physical Western Union agents, Paul has moved on from physical money transfer joints. He says that most Ugandans back home are unfamiliar with the process of sending money through Western Union and both him and the other party would have to look for a Western Union joint, which – in his opinion – is too costly and too much of a hassle. Instead, he asks people to make transfers to his Ugandan bank account, after which he transfers the money onto his Dutch bank account. According to him, it’s “still quite cumbersome”.

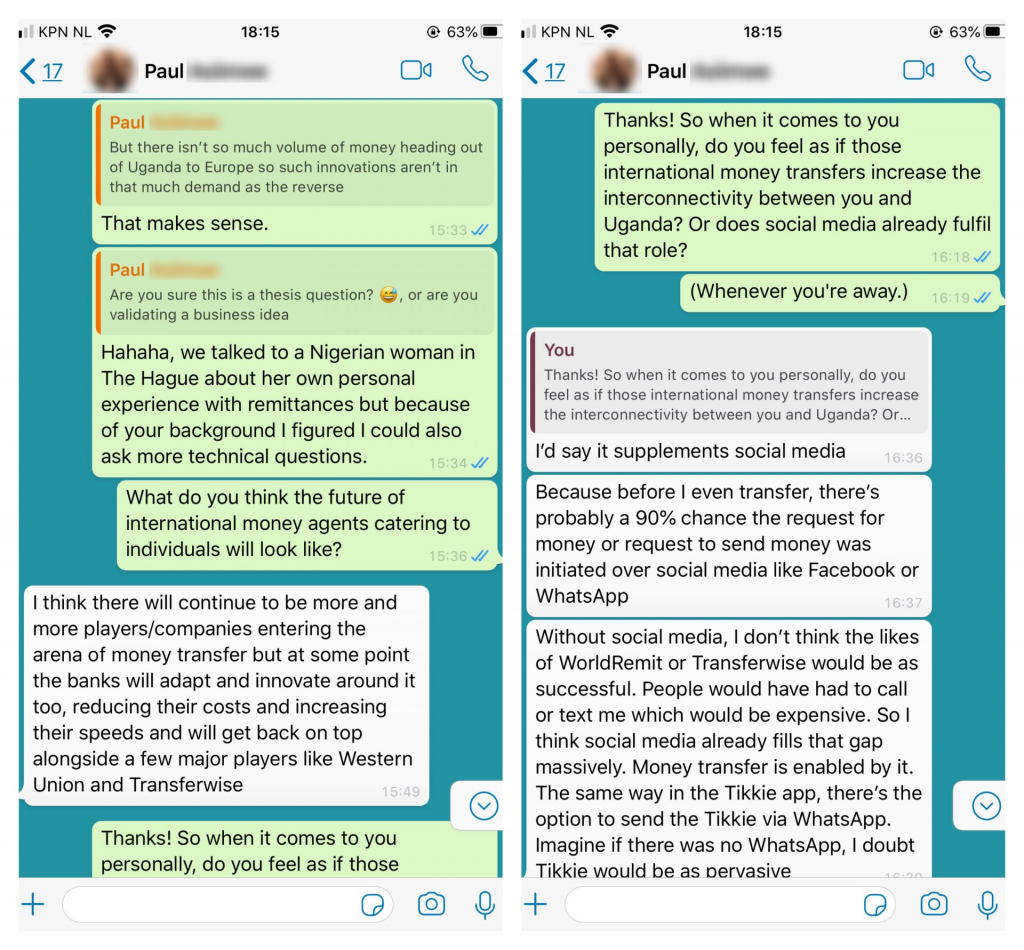

- He thinks the perfect solution to this would be a “payment/transfer app that allows withdrawing from the mobile money”, so that it would be easier to send payments from the African continent to the diaspora. However, the demand for such services is lower than the reverse, which means that innovations develop in a slower pace on this end.

- He expects that in time, there will be an increasing amount of businesses entering the arena of money transfers. At some point, Paul thinks that the banks will also adapt to these new developments and innovate by decreasing their costs and increasing the speed of financial transfers, which will make them capable of competing with major players in the field, such as TransferWise and Western Union.

- Abiola mentioned that she didn’t necessarily think that remittances increase the interconnectivity between her and Nigeria, as social media already fulfil that role. Paul however is of the opinion that remittances supplement social media: “Because before I even transfer, there’s a 90% chance the request for money or request to send money was initiated over social media like Facebook or WhatsApp.” He thinks that, without social media, money transfer services would not be as successful. Other wise, “(…) people would have had to call or text me which would be expensive.”

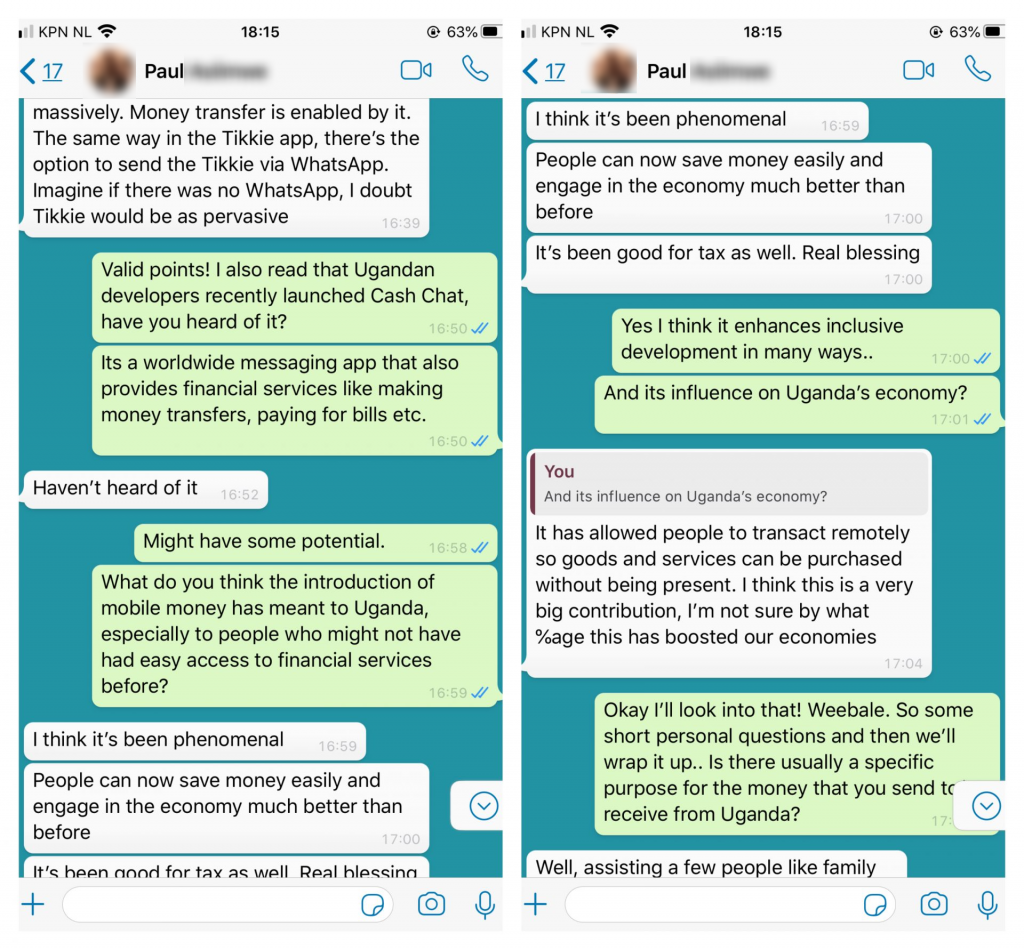

- Paul is of the opinion that the introduction of mobile money in Uganda (a service mostly provided by MTN, a mobile telecommunications company) has been “phenomenal”. It has made it far easier for people to save money and engage in the economy, therefore enhancing inclusive development.

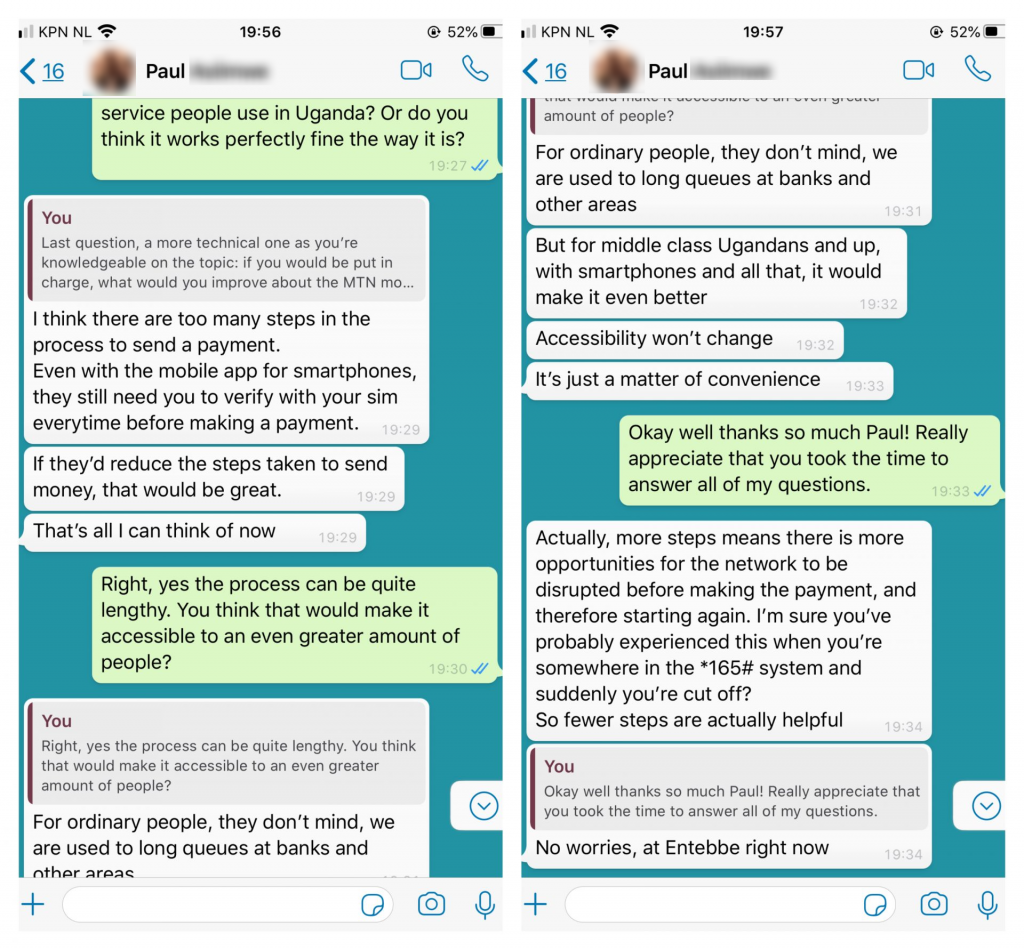

- Lastly, he thinks that the process of sending and receiving mobile money in Uganda could be made a little more convenient by reducing the amount of steps that need to be taken in order to send money, as the process can be quite lengthy. According to him, it would not necessarily increase accessibility, “(…) it’s just a matter of convenience”.

And an overview of all of our related posts:

1) Money Transfer Services in The Hague: An overview

2) Money Transfer Services in The Hague: Mapping the money transfer services

3) Money Transfer Services in The Hague: Abiola Adegoke on her experiences with remittances

4) Money Transfer Services in The Hague: Insights from an online survey